Advanced TV Revenue Share by Brand

AUSTIN, Texas (PRWEB)

April 28, 2020

Advanced TV revenues are forecast to grow by a 9% growth rate from 2019 to 2025 to $26 billion, according to the new DSCC Quarterly Advanced TV Shipment and Forecast Report, introduced this week and now available to subscribers. This report covers the worldwide premium TV market, including the most Advanced TV technologies: WOLED, QD Display, QDEF, Dual Cell LCD and MiniLED with 4K and 8K resolution. This report looks at current and future TV shipments and revenues by technology, region, brand, resolution and size, and forecasts the growth of all of these technologies. The report includes the preliminary shipment result for Q1 2020, a forecast by quarter for 2020 and an annual forecast to 2025.

Advanced TV is defined as any TV with an advanced display technology feature, including all OLED TVs, 8K LCD TVs and all LCD TVs with quantum dot technology. The historical data in the report allows analysis by feature for advanced LCD TVs, including:

- QDEF TV: TV using a Quantum Dot Enhancement Film; these TVs are sold as “QLED” by Samsung, TCL and others.

- MiniLED: LCD TVs with a MiniLED backlight, as sold by TCL starting in 2019.

- Dual Cell: LCD TVs employing dual-cell technology, as introduced by Hisense in 2019.

- LCD Others: this category includes LCD TVs with 8K resolution, that do not fall in any other category.

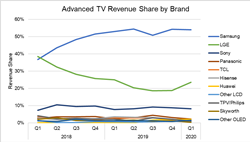

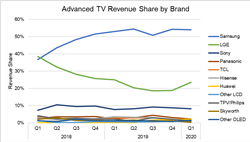

The report’s pivot tables allow analysis of brand share by screen size, region, technology, resolution and other variables. In Q1 2020, among all Advanced TV products Samsung increased its revenue share to 54% from 53% in Q1 2019 by expanding its QDEF product line into more affordable models. LG held the #2 brand position in Q1 2020 with 24% revenue share, while Sony took the third spot with 8%.

The PowerPoint report includes analysis of brand share by region and product segment, allowing a more focused view of brand share battles. The share battle in China has gotten increasingly intense, with four companies with double-digit % market share. Samsung’s share of Advanced TV in China increased to an all-time high in Q1 with 42% unit and revenue share and Huawei has emerged as a major player in Advanced LCD TVs, capturing an 18% share in Q1. Hisense introduced OLED TV in 2019, but this did not prevent the company’s share from eroding to 14% in Q1. LGE fares poorly in China with less than a 5% share. Skyworth, once a major player with 24% share in Q2 2018, has seen its position diminish to only 3% share in Q1 2020.

The report allows detailed analysis of historical shipment patterns, but also provides DSCC’s forecast of technology, product and pricing. While the COVID-19 impact will slow growth in Q2 2020 to 11% Y/Y, growth will resume in the second half of 2020 and Q4 unit growth will reach 27% Y/Y. 48” OLED will start in limited volumes, adding to the product mix for OLED, and LGD’s increasing OLED capacity will allow OLED to hold its unit share of Advanced TV and increase OLED’s revenue share. Across all technologies and sizes, we expect Advanced TV unit shipments to increase by 30% in 2020 compared to 2019.

Turning to the long-term forecast, we expect that Advanced TV shipments will grow from less than 10 million in 2019 to nearly 35 million in 2025, a 24% CAGR for that time period. OLED TV units are expected to grow at a 31% CAGR from 2019-2025 to 14.7 million units, while advanced LCD TV units are expected to grow at a 21% CAGR to 20.8 million units. The largest sizes will see the biggest growth, with growth in 75”+ expected to be 36%, and growth in 75”+ OLED even higher at 87% CAGR.

From a revenue standpoint, while the overall category will see revenue growth, OLED TV is expected to capture all the revenue growth in Advanced TV, as advanced LCD revenues are expected to be the same in 2025 compared to 2019. OLED TV revenues are expected to grow at a 19% CAGR from 2019-2025 to $16.2 billion. Advanced LCD TV revenues were $10.0 billion in 2019, are expected to peak at $11.1 billion in 2022-2023, then decline to $10.0 billion by 2025. Even larger size LCD TVs are not expected to have revenue growth as Samsung shifts its emphasis from its “QLED” LCD products to QD OLED.

DSCC’s Quarterly Advanced TV Shipment and Forecast Report includes technical descriptions of all major Advanced TV display technologies, plus quarterly shipment results from Q1 2018 through Q1 2020 preliminary results, sortable by technology, region, brand, resolution and size, and includes pivot tables for analysis of units, revenues, ASPs and other metrics. The report includes DSCC’s quarterly forecast for the current year plus an annual forecast for five years across technology, region, resolution and size. Readers interested in subscribing to the DSCC Quarterly Advanced TV Shipment Report should contact gerry@displaysupplychain.com.

About Display Supply Chain Consultants (DSCC)

Display Supply Chain Consultants (DSCC) was formed by experienced display market analysts from throughout the display supply chain and delivers valuable insights through consulting, syndicated reports and events. The company has offices in Korea, China, Japan and the US, is on the web at https://www.displaysupplychain.com and can be reached in the US at info@displaysupplychain.com and (512) 577-3672.

Share article on social media or email: